July 24, 2018

Postal Banking is Successful Around the World – Could It Work Here?

![]()

(This article first appeared in the July-August 2018 issue of The American Postal Worker magazine)

Postal services across the world provide tried and tested and successful models for postal banking, or the provision of financial services via the post. New research by Holly Feldman Wiencek, Research Assistant at the National Association of Letter Carriers (NALC), shows differing models for postal banking across the world and the factors that drive their success.

While services and how they are provided vary, 91 percent of postal services worldwide offer financial services, serving 1.5 billion people. According to the Universal Postal Union, this makes the postal sector the second largest contributor to financial inclusion worldwide,” right behind the banking industry. Financial inclusion is the idea of increasing access to banking services for people who have traditionally been excluded. The concept of postal banking is not new to these shores. During the first half of the twentieth century, the United States Postal Savings System was a great promoter of financial inclusion, especially or new immigrants.

In some countries, the postal service rents out space to third-party providers and in others, the post operates under its own banking license. The United Kingdom’s Post Office Money, for example, is operated by Post Office Ltd., the government-owned retail side of the UK’s postal service. It offers services in partnership with a financial services provider, most commonly the Bank of Ireland UK. In France, Banque Postale is a whollyowned subsidiary of La Poste, the national postal service in France, and it operates under its own universal banking license.

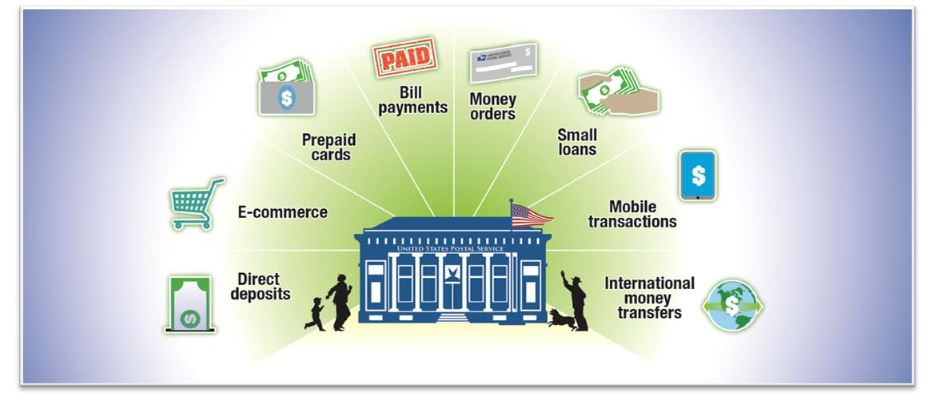

in place. From a report by the USPS OIG, January 2014.

The management of Poste Italiane, the national postal provider in Italy, surveyed models of postal banking around the world and identified three key factors that determine the success of a postal bank. The first is the postal network itself. The report finds that “Posts that have broad networks and infrastructures, have control over their networks, and maximize the use of their networks had more success because they are able to reach more potential customers.”

This is good news for the potential of postal banking in the United States. The U.S. Postal Service, with more than 30,000 retail locations, is the world’s largest retail network. And many of those post offices are located in bank deserts. Fifty-nine percent of post offices are in zip codes with zero banks or just one bank branch. The U.S. Postal Service is geographically well-positioned to reach people with little-to-no access to retail banking services.

The second factor the Poste Italiane study identified was the strength of the postal service brand. They found that many postal services worldwide are “seen as more reliable, convenient, transparent, and safe than private banks.” This is more good news, as Americans consistently rank the USPS highest among all federal agencies. More than 70% of respondents rate USPS performance “excellent” or “good.” Our public postal service enjoys much higher public confidence than banks or payday lenders.

Finally, Poste Italiane’s study recommends that postal services respond to the needs of the people in their country with the right products. That’s why the APWU has joined with the Campaign for Postal Banking. We’ve been working with unions, consumer rights and civil rights groups, financial reform organizations and people who’ve been fighting back against banks that serve Wall Street and the predatory lenders that rip off our communities. We’re pushing the U.S. Postal Service to leverage its strong infrastructure and its mission to provide reliable, low-cost financial services that the people of this country need, want and deserve.